Is there any equilibrium point in housing market, considering the many factors influencing demand and supply?

The

main determinants of the demand for housing are demographic. Population

size and population growth are the core demographic variables. However,

family size, the age composition of the family, the number of children,

net migration, non-family household formation, the number of double

family households, death rates, divorce rates, and marriages are other

demographic variables that would influence demand for housing. Other

factors such as household income, price of housing, cost, availability

of credit, consumer preferences, investor preferences, price of

substitutes and price of complements all play a role in determining

demand for housing.

Income is an important determinant of demand

as shown by a study conducted by De Leeuw in 1971 that showed positive

income elasticity of demand in North America ranging from 0.5 to 0.9,

meaning the market demand for housing grew as real income rose. The

price of housing is also an important variable influencing demand for

housing, where in terms of elasticity just like any normal goods it is

negative increase in price will result in decrease in demand.

As

for supply, the quantity of incoming supply is typically influenced by

cost, price of existing stock of houses, and the technology used in the

construction, where material costs tend to contribute the largest share

of the construction cost, about 30% to 40%. In the short run, supply

tends to be very price inelastic increase in cost will have less effect

on supply. However, over a longer period, it tends to be very price

elastic increase in cost will lower supply.

A study conducted by

Fallis in 1985 showed price elasticity of supply was estimated at 8.2,

indicating increased in cost would lower supply significantly. The

degree of elasticity depends on the elasticity of substitution and

supply restrictions. For example, the use of capital intensive

technology has been employed to reduce the rising labour cost, thus

having less impact on the supply of housing.

As at first half of

2011, Malaysia had 4,466,062 units of housing, an increase of 1.7% from

the total of supply in the first half of 2010. About 24,709 units were

completed in the first half of 2011, a lower number compared to 50,611

units completed in the first half of 2010. Kuala Lumpur and Selangor

accounted for 6,567 units or 27% of the total new stock. Kuala Lumpur

and Selangor had 414,436 and 1,285,192 homes, reflecting an increase of

2.0% and 1.7% respectively from the total as of first half of 2010.

Other

states which showed significant number of units completed are Sarawak

(2,612), Penang (2,507) and Perak (2,184). The incoming supply in the

country was recorded at 560,636 units, where Selangor is the largest

contributor (134,143 or 24% of the total) followed by Johor (76,429 or

14%) and Negri Sembilan (65,227). Kuala Lumpur has 39,656 units coming

on stream.

In terms of transactions recorded as of first half of

2011 for the country, there were 133,984 transactions in the residential

category, out of which the largest transacted numbers were priced in

the range of RM100,000 to RM150,000, which accounted for 22,857 units,

followed by units priced between RM250,000 and RM500,000, which

accounted for 21,559 units.

Selangor recorded the highest number

of transactions at 38,424 units, followed by Johor (15,015 units),

Penang (13,832 units), and Kuala Lumpur (11,522 units). The most popular

units transacted in Selangor, Kuala Lumpur, and Penang were for units

priced between RM250,000 and RM500,000, while in Johor, the highest

transactions recorded were for units priced between RM100,000 and

RM150,000.

This brief analysis gives an indication that the total

number of units coming into the market needs to be in line not only

with the level of affordability of potential buyers in the area the

projects are to be launched but also the demographics of Malaysian

population.

As of July 2010, total population was estimated to be

28.25 million and the population is expected to grow at a rate of 2.4%

per annum, where about 65% of the population is urban population. Today,

less than 4% of Malaysians live in poverty and it is estimated that

about 2.0% of the total urban population in Malaysia lives below the

poverty line, earning monthly household income of equal or less than

RM750. Low income households (earning income equal or less than RM2,000

per month) represents 75% of the median income in Malaysia.

The

national average household income is estimated at RM4,000 per month. It

should also be noted that about 65% of Malaysia's population is below

the age of 35, thus there would definitely be strong demand for housing.

Due

to continuous movement in the factors affecting supply and demand for

housing, policy intervention is necessary to ensure that the majority of

the population has equal access to own homes. Singapore's public

housing policy is often cited as the most successful example of

affordable housing provision in Asian cities. A study conducted in 2000

estimated that about 85% of the total population lived in public housing

with nearly 95% of them owning the flats they occupied.

By

centralising its public housing effort under a single authority, Housing

Development Board, Singapore has circumvented the typical problems of

duplication and fragmentation of duties, and bureaucratic rivalries

associated with multi-agency implementation. This centralised function

also serves as a mechanism to ensure supply and demand are checked.

It

is hoped that the provision of affordable homes as announced in Budget

2012 would achieve its main objective of increasing home ownership among

the majority of the population.

Senator Datuk Abdul Rahim Rahman is the executive chairman of Rahim & Co group of companies. - By Datuk Abdul Rahim Rahman (

The Star)

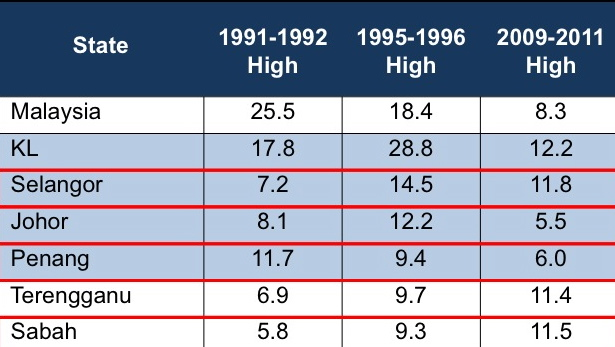

In

this current article, we will be highlighting on Penang. In summary, it

can be said that Penang, as a whole is experiencing a healthy property

market, with prices increasing on an average of 6% for the period of

2009 to 2011. In comparison with the highs of 1995-1996 and 1992-1992,

6.0% capital appreciation is relatively low, and doesn’t show an

unsustainable growth for the state of Penang.

In

this current article, we will be highlighting on Penang. In summary, it

can be said that Penang, as a whole is experiencing a healthy property

market, with prices increasing on an average of 6% for the period of

2009 to 2011. In comparison with the highs of 1995-1996 and 1992-1992,

6.0% capital appreciation is relatively low, and doesn’t show an

unsustainable growth for the state of Penang. Let’s

look at Penang’s standing in the national standings, referencing the

average house prices in the country. Looking at the statistics, Penang’s

prices are at an average of RM232k. Comparing this with the national

average of RM209k per unit, Penang is among the other states where

property prices are higher than the national average.

Let’s

look at Penang’s standing in the national standings, referencing the

average house prices in the country. Looking at the statistics, Penang’s

prices are at an average of RM232k. Comparing this with the national

average of RM209k per unit, Penang is among the other states where

property prices are higher than the national average. The

final chart we would like to highlight would be the property prices in

Penang Island as compared to the mainland. Looking at the chart below,

if you were to do a comparison study with regards to the prices, since

1999, until 3rd quarter 2011, you will notice that the appreciation of

residential property prices have been significantly higher in the island

state as compared to the mainland. Residential properties in the island

state have seen a substantial growth exceeding 100%, since 2001.

The

final chart we would like to highlight would be the property prices in

Penang Island as compared to the mainland. Looking at the chart below,

if you were to do a comparison study with regards to the prices, since

1999, until 3rd quarter 2011, you will notice that the appreciation of

residential property prices have been significantly higher in the island

state as compared to the mainland. Residential properties in the island

state have seen a substantial growth exceeding 100%, since 2001.